Generally, new technologies are forcing governments to be particularly considerate to time. In order to make right decision and avoid falling behind, governments must identify and resolve the different issues that have arisen from the transaction period during which traditional and e-government co-exist. Government should guide and control the transformation of government into e-government rather than just focusing on introduction of ICTs. Meanwhile, the use of ICT to strengthen the involvement of citizens and businesses in public decision must be progress at the same time.

The Electronic Government initiative in Malaysia was launched to lead the country into the Information Age. It has improved both how the government operates internally as well as how it delivers services to the people of Malaysia. It seeks to improve the convenience, accessibility and quality of interactions with citizens and businesses; simultaneously, it will improve information flows and processes within government to improve the speed and quality of policy development, coordination and enforcement.The vision of Electronic Government is avision for government, businesses and citizenry working together for the benefit of Malaysia and all of its citizens. The vision focuses on effectively and efficiently delivering services from the government tothe people of Malaysia, enabling the government to become more responsive to the needs of its citizens.

The 7 pilot projects of the ElectronicGovernment Flagship Application are as follows:

1. Project Monitoring System (SPP II)

2. Human Resource ManagementInformation System (HRMIS)

3. Generic Office Environment (GOE)

4. Electronic Procurement (EP)

5. Electronic Services (E-Services)

6. Electronic Labour Exchange (ELX)

7. E-Syariah

The my Government Portal (www.gov.my)acts as the one-stop source of Malaysian government information and services for the citizens.

The recent survey about the e-goverment adoption in Malaysia, which was done by the market information group TNS, indicated that the e-goverment use is growing but a slow pace.

The malaysians are also concerned about the security of doing transactions over the Internet and this resulted in low usage of e-goverment services.

As far as the age group is concerned, the younger Malaysian who are under 34, are the primary users of e-goverment services. in the survey also state that households with high income and higher levels of education actively use the e-goverment services.

E-goverment merging field, which is rapidly gaining attention and importance. Citizens expect and demand governmental services with a high degree of quality, quantity, and availability in a 24-hour, seven-days-a-week, and year-round fashion.

Governments are developing information systems and electronic services that have the capacity to meet these emerging service needs and demands of citizens and other clients. Success in delivering electronic services depends upon the capability and self-confidence of citizens in performing e-transactions, as well as their trust and confidence in the protection of their personal data within an open and accountable government.

The ease of use, compatibility, and trustworthiness are significant predictors of citizens's tention to use e-Services and that perceived reactive advantage, perceived image, perceived compatibility, perceived usefulness, and relative advantage are significant elements of e-goverment adoption.

Sunday, March 15, 2009

Credit Card Debt : causes and prevention

Credit Card Debt is the unpaid balance on the credit card. This is not the minimum amount due, but is the total balance due on a respective line of credit. When the consumers has been late on a payment or does not pay the bank on time for that the money he or she has spent. Then, the bank will charge a late payment penalty and increases via interest on the amount of debt the consumer has.

Nowadays, credit card debts are major cause of bankruptcies each year. It is because many people have never realized of its consequences from financial and non financial perspectives when get a new credit card or not enough safety net when there is an incident happen.

The following is the main reason of the credit card debt:

POOR MONEY MANAGEMENT

A monthly spending plan is essential. But they does not know where their money is going, do not know what is the percentage of their income have they saved each and every month. Thus, it has lead to a rise in debts by using credit cards. Then, they cannot set aside money for saving and emergency needs.

GAMBLING

Today, gambling is fun and entertaining but it will be hard to stop when it becomes addictive. Thus, it will surely lead to a financial disaster if borrowing money through credit card for gambling.

UNEMPLOYMENT

People are forced to use credit card for expenses purposes to maintain current lifestyle. When the main breadwinner of the household has loss his job and could not find a new job during short periods. This may lead to a rise in debt when expenses are not cut down in line with the reduction in income.

EXCESSIVE MEDICAL EXPENSES

Credit card will probably become one of the sources of funds to pay off the medical expenses if health insurance is not adequate to cover the medical bills if one of your family members suffers serious illness.

The following is the ways to prevent credit card debt:

BUDGET

List all monthly bills and necessities and make sure that you can meet all the basic necessities that you spent and stay within your budget guidelines. this will prevent from overspending and fall under deeper debt load.

SELF CONTROL AND DISCIPLINE

One of the best practices is to have a direct set up so that able to pay back the full amount each month and use in emergencies. Thus, self control and discipline to keep these cards in wallet and would not overspend. The

CAUTION ABOUT AGREEMENT

make sure you have read word by word in all the agreements before u signed and make a payment. Sometimes, there could be hidden some fees that we does not need to pay.

Nowadays, credit card debts are major cause of bankruptcies each year. It is because many people have never realized of its consequences from financial and non financial perspectives when get a new credit card or not enough safety net when there is an incident happen.

The following is the main reason of the credit card debt:

POOR MONEY MANAGEMENT

A monthly spending plan is essential. But they does not know where their money is going, do not know what is the percentage of their income have they saved each and every month. Thus, it has lead to a rise in debts by using credit cards. Then, they cannot set aside money for saving and emergency needs.

GAMBLING

Today, gambling is fun and entertaining but it will be hard to stop when it becomes addictive. Thus, it will surely lead to a financial disaster if borrowing money through credit card for gambling.

UNEMPLOYMENT

People are forced to use credit card for expenses purposes to maintain current lifestyle. When the main breadwinner of the household has loss his job and could not find a new job during short periods. This may lead to a rise in debt when expenses are not cut down in line with the reduction in income.

EXCESSIVE MEDICAL EXPENSES

Credit card will probably become one of the sources of funds to pay off the medical expenses if health insurance is not adequate to cover the medical bills if one of your family members suffers serious illness.

The following is the ways to prevent credit card debt:

BUDGET

List all monthly bills and necessities and make sure that you can meet all the basic necessities that you spent and stay within your budget guidelines. this will prevent from overspending and fall under deeper debt load.

SELF CONTROL AND DISCIPLINE

One of the best practices is to have a direct set up so that able to pay back the full amount each month and use in emergencies. Thus, self control and discipline to keep these cards in wallet and would not overspend. The

CAUTION ABOUT AGREEMENT

make sure you have read word by word in all the agreements before u signed and make a payment. Sometimes, there could be hidden some fees that we does not need to pay.

Monday, March 9, 2009

Review a local e-commerce site

Lelong Malaysia is a website that provides easy malaysian auction and online shopping which includes trading of computers, cars, houses, electronics, sports, antique, software and handphone. The website also offers online payment transaction.

Lelong Malaysia is a website that provides easy malaysian auction and online shopping which includes trading of computers, cars, houses, electronics, sports, antique, software and handphone. The website also offers online payment transaction.The website is unique because the auctioned items are rare and awesome such as these weird stuff and spy camera detector pen, which allows users to detect any spy devices around on a certain location.

The website also auctions popular products from other website including MaxAudio Online, which is a premier Car Audio, Video, Accessories & Performance Online Store.

Lelong offers each merchant member a page where they can sell their products such as Shinoz's Online Store which is powered by Lelong.

The Lelong Forum allows members to interact with each other and ask questions. Other members could provide a answers and recommendations about issues related to Lelong and transportation of bought materials which have problems with the courier service.

Members at Webmaster Malaysia Forum even featured the lelong's service. The free auction, free membership, free bidding, free banner advertisement and free trading. Sylok.com's Forum also featured Lelong's Bank Auctioning and Photomalaysia Community.

As more and more small and medium business "go online" using e-commerce website such as lelong. People have provided guides such as Lelong Malaysia Auction Online Guide that are listed on lelongmalaysia.com.

The popularity of the site caused the growth of other websites such as Malaysia Auction Lelong Property (real estate), Cari Rumah Sewa, Malaysia Auction Online and Iklan Malaysia.

Monday, March 2, 2009

mobile payment system in malaysia its potentials and consumers adoption strategies

A mobile payment or m-payment may be defined, for our purposes, as any payment where a mobile device is used to initiate, authorize and confirm an exchange of financial value in return for goods and services. Mobile devices may include mobile phones, PDAs, wireless tablets and any other device that connect to mobile telecommunication network and make it possible for payments to be made. The realization of mobile payments will make possible new and unforeseen ways of convenience and commerce. Unsuspected technological innovations are possible. Music, video on demand, location based services identifiable through mobile handheld devices – procurement of travel, hospitality, entertainment and other uses are possible when mobile payments become feasible and ubiquitous. Mobile payments can become a complement to cash, cheques, credit cards and debit cards. It can also be used for payment of bills (especially utilities and insurance premiums) with access to account-based payment instruments such as electronic funds transfer, Internet banking payments, direct debit and electronic bill presentment.

A mobile payment or m-payment may be defined, for our purposes, as any payment where a mobile device is used to initiate, authorize and confirm an exchange of financial value in return for goods and services. Mobile devices may include mobile phones, PDAs, wireless tablets and any other device that connect to mobile telecommunication network and make it possible for payments to be made. The realization of mobile payments will make possible new and unforeseen ways of convenience and commerce. Unsuspected technological innovations are possible. Music, video on demand, location based services identifiable through mobile handheld devices – procurement of travel, hospitality, entertainment and other uses are possible when mobile payments become feasible and ubiquitous. Mobile payments can become a complement to cash, cheques, credit cards and debit cards. It can also be used for payment of bills (especially utilities and insurance premiums) with access to account-based payment instruments such as electronic funds transfer, Internet banking payments, direct debit and electronic bill presentment.  A mobile payment service in order to become acceptable in the market as a mode of payment the following conditions have to be met :

A mobile payment service in order to become acceptable in the market as a mode of payment the following conditions have to be met :a) Simplicity and Usability: The m-payment application must be user friendly with little or no learning curve to the customer. The customer must also be able to personalize the application to suit his or her convenience.

b) Universality: M-payments service must provide for transactions between one customer to another customer (C2C), or from a business to a customer (B2C) or between businesses (B2B). The coverage should include domestic, regional and global environments. Payments must be possible in terms of both low value micro-payments and high value macro-payments.

c) Interoperability: Development should be based on standards and open technologies that allow one implemented system to interact with other systems.

d) Security, Privacy and Trust: A customer must be able to trust a mobile payment application provider that his or her credit or debit card information may not be misused. Secondly, when these transactions become recorded customer privacy should not be lost in the sense that the credit histories and spending patterns of the customer should not be openly available for public scrutiny. Mobile payments have to be as anonymous as cash transactions. Third, the system should be foolproof, resistant to attacks from hackers and terrorists. This may be provided using public key infrastructure security, biometrics and passwords integrated into the mobile payment solution architectures.

e) Cost: The m-payments should not be costlier than existing payment mechanisms to the extent possible. A m-payment solution should compete with other modes of payment in terms of cost and convenience.

f) Speed: The speed at which m-payments are executed must be acceptable to customers and merchants.

g) Cross border payments: To become widely accepted the m-payment application must be available globally, word-wide.

Malaysian Electronic Payment System (1997) Sdn Bhd is a payment consortium owned equally by 12 local banks. Its subsidiary companies are MEPS Currency Management Sdn Bhd (MCM) and FPX Gateway Sdn Bhd (FPX).

MEPS plays a role in the implementation of smart card for Automated Teller Machine (ATM) card, which is an upgrade to chip-based card from previous magnetic-stripe card issued to all banks customer.

MEPS plays a role in the implementation of smart card for Automated Teller Machine (ATM) card, which is an upgrade to chip-based card from previous magnetic-stripe card issued to all banks customer.

The card is also known as Bankcard, a card with multiple functions. There are three main functions that can be used namely ATM (with various combinations of banking transactions), e-Debit (online purchase payment) transactions at participating merchants and MEPS Cash (load in a monetary value into your Bankcard chip) and pay of participating merchants.

MEPS provides the following services in its network to all participating banks:

1.Shared Nationwide ATM Network, provides the switch which enable bank customers to conveniently access their funds anywhere from any of the participating banks’ ATMs.

2.Shared Regional ATM Network, a cross-border ATM link with Indonesia (ArtaJasa, Rintis), Singapore (NETS), Thailand (ITMX) and China (CUP) that offers participating banks’ customers the convenience of making cash withdrawals via ATM in the said countries and vice versa.

3.e-Debit, enables the purchase amount to be immediately deducted from the savings or current account direct into the retailer's or merchant's bank account. This provides consumers with better cash management and peace of mind as all transactions are PIN based. In addition, the new card is embedded with a sophisticated, tamper-resistant smart chip to protect consumers against the risk of fraud.

4.Mobile Prepaid Top-Up via ATM, offers more convenience for mobile phone subscribers to top-up through MEPS’ ATMs.

5.Interbank ATM Fund Transfer (IBFT), allows bank customers to transfer funds from one account to another account in another bank. The beneficiary will receive the funds immediately and instantaneously, as the transfer is online and in real-time.

6.Interbank GIRO (IBG), makes interbank funds transfer more convenient to bank customers via an electronic channel. It enables payments to be made without the need to raise physical supporting vouchers or documents such as cheques, bank drafts, etc. It is an interbank fund transfer system that facilitates payments and collections via the exchange of digitized transactions between banks. For corporations, it is ideal for high volume interbank payments up to a maximum of RM100,000 per transaction such as payroll and dividend/warrant payments. As for individuals, it is ideal for transactions such as credit card payments and loan repayments. It offers bank customers, be an individual or corporation, a secure interbank fund transfer system/channel for all sorts of payments through direct debiting of the customers' account(s) and crediting into the beneficiaries account; with any IBG participating banks.

7.Financial Processing Exchange (FPX), opens new doors for e-Commerce, in particular business to business (B2B) and business to commerce (B2C) payments. FPX is an alternative payment channel for customers to make payment at e-market places such as websites and online stores as well as for corporations to collect bulk payment from their customers. It leverages on the Internet banking services of participating banks and provides fast, secure, reliable, real-time online payment processing. FPX provides complete end-to-end business transactions, resourceful payment records, simplified reconciliation and reduced risks as fund movements are between established financial institutions.

Saturday, February 28, 2009

Things to take note to prevent e-auction fraud when a consumer participating in an e-auction

Internet auction fraud is a growing epidemic worldwide, as online shopping has grown significantly every year that online shopping has been available. 51,000 cases of internet fraud cases were reported in 2002. In 2006, that number ballooned to 97,000. The numbers are staggering, but everyone can lower their risk by knowing what auction fraud is, how to detect it, and how to prevent falling for it.

Most internet auction fraud cases involve straightforward scams where consumers allegedly win merchandise by being the highest bidder. All sounds good until they send the payment and never receive the merchandise.

Some of the ways people can prevent e-auction fraud is by:

1. User identity verification such in IC number, driver’s license number or date of birth. For example, verified eBay user, the voluntary program, encourages users to supply eBay with information for online verification.

2. Authentication service. It is to determine whether an item is genuine and described appropriately. It difficult to perform because their training and experience, experts can detect counterfeits based on subtle detail.

3. Grading services which is a way to determine the physical condition of an item, such as ‘poor quality’ or ‘mint condition’. Different item have different grading systems. For example, trading cards are graded from A1 to F1, while coins are graded from poor to perfect uncirculated.

4. Feedback forum. It allows buyers and sellers to build up their online trading reputations. It provides user with ability to comment on their experiences with other.

5. Insurance policy. For example, eBay offers insurance underwritten, users are covered up to $200, will with a $25 deductible. The program is provided at no cost to eBay user.

6. Escrow services. Both buyers and sellers in a deal are protected with an independent third party. Buyer mails the payment to escrow services which verifies the payment and alerts the seller when everything checks out. An example of a provider of online escrow services s i-Escrow.

7. Non-payment punishment. To protect sellers, a friendly warning for first-time nonpayment. A sterner warning is for second-time offense, with a 30 day suspension for a third offense and an indefinite suspension for a fourth offense.

8. Appraisal services which use a variety of methods to appraise items. It includes expert assessment of authenticity and condition, and reviewing what comparable items have sold for in the marketplace in recent months.

9. Item verification which is a way of confirm he identity and evaluate the condition of an item. Third parties will evaluate and identify an item through a variety of means. For example, some collectors have their item “DNA tagged” for identification purpose. It provides a way of tracking an item if it charges ownership in future.

10. Physical inspection. It can eliminate many problems especially for collectors’ item

Most internet auction fraud cases involve straightforward scams where consumers allegedly win merchandise by being the highest bidder. All sounds good until they send the payment and never receive the merchandise.

Some of the ways people can prevent e-auction fraud is by:

1. User identity verification such in IC number, driver’s license number or date of birth. For example, verified eBay user, the voluntary program, encourages users to supply eBay with information for online verification.

2. Authentication service. It is to determine whether an item is genuine and described appropriately. It difficult to perform because their training and experience, experts can detect counterfeits based on subtle detail.

3. Grading services which is a way to determine the physical condition of an item, such as ‘poor quality’ or ‘mint condition’. Different item have different grading systems. For example, trading cards are graded from A1 to F1, while coins are graded from poor to perfect uncirculated.

4. Feedback forum. It allows buyers and sellers to build up their online trading reputations. It provides user with ability to comment on their experiences with other.

5. Insurance policy. For example, eBay offers insurance underwritten, users are covered up to $200, will with a $25 deductible. The program is provided at no cost to eBay user.

6. Escrow services. Both buyers and sellers in a deal are protected with an independent third party. Buyer mails the payment to escrow services which verifies the payment and alerts the seller when everything checks out. An example of a provider of online escrow services s i-Escrow.

7. Non-payment punishment. To protect sellers, a friendly warning for first-time nonpayment. A sterner warning is for second-time offense, with a 30 day suspension for a third offense and an indefinite suspension for a fourth offense.

8. Appraisal services which use a variety of methods to appraise items. It includes expert assessment of authenticity and condition, and reviewing what comparable items have sold for in the marketplace in recent months.

9. Item verification which is a way of confirm he identity and evaluate the condition of an item. Third parties will evaluate and identify an item through a variety of means. For example, some collectors have their item “DNA tagged” for identification purpose. It provides a way of tracking an item if it charges ownership in future.

10. Physical inspection. It can eliminate many problems especially for collectors’ item

The application of pre-paid cash card for consumers

Pre-paid cash card means reloading funds or cash into the particular card and using it as any normal credit card or debit card. The difference is that the user can manage his/her financial spendings more efficiently. User who utilize this type of cards do not have to worry on interest rates at the end of the month.

It is considered as most secure and safe financial transaction card because can it likes a portable access point to checking account. Nevertheless, it could not use for online shopping and in “quick pay” terminals that have a card reader but no keypad to enter a personal identification number.

The following are some of the examples of prepaid cards offered by card institutions.

It is considered as most secure and safe financial transaction card because can it likes a portable access point to checking account. Nevertheless, it could not use for online shopping and in “quick pay” terminals that have a card reader but no keypad to enter a personal identification number.

The following are some of the examples of prepaid cards offered by card institutions.

How to safeguard our personal and financial data?

Today's world of technological advances and virtual everything - banking, bill paying, etc. - it's more important than ever to make sure we protect our personal data. In recent years, the Internet has become an appealing place for criminals to obtain identifying data, such as passwords or even banking information. In their haste to explore the exciting features of the Internet, many people respond to "spam" - unsolicited e-mail - that promises them some benefit but requests identifying data, without realizing that in many cases, the requester has no intention of keeping his promise. In some cases, criminals reportedly have used computer technology to obtain large amounts of personal data.

Today's world of technological advances and virtual everything - banking, bill paying, etc. - it's more important than ever to make sure we protect our personal data. In recent years, the Internet has become an appealing place for criminals to obtain identifying data, such as passwords or even banking information. In their haste to explore the exciting features of the Internet, many people respond to "spam" - unsolicited e-mail - that promises them some benefit but requests identifying data, without realizing that in many cases, the requester has no intention of keeping his promise. In some cases, criminals reportedly have used computer technology to obtain large amounts of personal data.  With enough identifying information about an individual, a criminal can take over that individual's identity to conduct a wide range of crimes: For example, false applications for loans and credit cards, fraudulent withdrawals from bank accounts, fraudulent use of telephone calling cards, or obtaining other goods or privileges which the criminal might be denied if he were to use his real name. If the criminal takes steps to ensure that bills for the falsely obtained credit cards, or bank statements showing the unauthorized withdrawals, are sent to an address other than the victim's, the victim may not become aware of what is happening until the criminal has already inflicted substantial damage on the victim's assets, credit, and reputation.

With enough identifying information about an individual, a criminal can take over that individual's identity to conduct a wide range of crimes: For example, false applications for loans and credit cards, fraudulent withdrawals from bank accounts, fraudulent use of telephone calling cards, or obtaining other goods or privileges which the criminal might be denied if he were to use his real name. If the criminal takes steps to ensure that bills for the falsely obtained credit cards, or bank statements showing the unauthorized withdrawals, are sent to an address other than the victim's, the victim may not become aware of what is happening until the criminal has already inflicted substantial damage on the victim's assets, credit, and reputation.To reduce or minimize the risk of becoming a victim of identity theft or fraud, there are some basic steps you can take. For starters, remember the word SCAM:

S: Be Stingy about giving out your personal information to others unless you have a reason to trust them, regardless of where you are.

C: Check your financial information regularly, and look for what should and shouldn't be there.

A: Ask periodically for a copy of your credit report.

M: Maintain careful records of your banking and financial accounts

S: Be Stingy about giving out your personal information to others unless you have a reason to trust them, regardless of where you are.

C: Check your financial information regularly, and look for what should and shouldn't be there.

A: Ask periodically for a copy of your credit report.

M: Maintain careful records of your banking and financial accounts

This below is the 10 ways to safeguard our personal and financial data

This below is the 10 ways to safeguard our personal and financial data1. Take Stock. Know what personal information you have in your files and on yourcomputers. Never leave sensitive papers in a common area unattended.

2. Scale Down. Keep only what you need for your business. If you don't have alegitimate business need for information, don't collect it.

3. Lock It. Protect the information that you keep. Limit access to employees with alegitimate business need. Control who has a key, the number of keys and knowwhen information is being accessed.

4. Pitch it. Properly dispose of what you no longer need. If you collect applicationswith personal financial information, make sure the paperwork is unreadablebefore you dispose of it. Crosscutshredding is an effective way to preventidentity thieves from stealing it from your trash.

5. Email Restrictions. Regular email is not a secure method for sending sensitivedata. Never send personal financial information via Email.

6. Protect It. Use antivirusand antispywaresoftware, as well as a firewall, andupdate them all regularly. Also, use a passwordactivatedscreen saver to lockyour screen whenever you are not in front of it.

7. Use "Strong" Passwords. The longer the password, the better. Use passwordswith a mix of letters, numbers & characters and frequently change yourpassword. Do not use the same password for all of the various accounts youaccess with a password.

8. Limit Team Roles. Only allow certain employees to access sensitive personalfinancial information wherever it is. Manage the user permission of youremployees carefully on places like the Member Solutions or banking websites.

9. Make Sure Your Vendors are PCI Compliant. Any financial institution,software provider, merchant processor, or other company that you do businesswith should be taking steps to be PCI compliant. Any company or softwareapplication that contains cardholder data must comply.

10. Treat it Like it Was Your Own. Safeguard all personal financial information ofyour customers, employees or anyone else like is was your own personalinformation.

Even though financial institutions are required to maintain copies of your checks, debit transactions, and similar transactions for five years, you should retain your monthly statements and checks for at least one year, if not more. If you need to dispute a particular check or transaction, especially if they purport to bear your signatures, your original records will be more immediately accessible and useful to the institutions that you have contacted.

Wednesday, February 25, 2009

Phishing: Examples and its prevention method

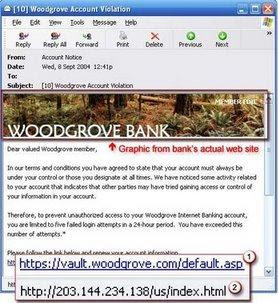

Phishing is a process of illegally acquiring personal and sensitive information from people such as credit card information, usernames and passwords. They may seem like web sites from a trustworthy entity but in fact, as soon as the victim inputs his or her information the phishing site will record all of the information and will exploit those information to fraud on the victim.

An example of a phishing site.

Ways to prevent phishing scams: Incorrect company name. Often the web address of a phishing site looks correct, but actually contains a common misspelling of the company name or a character or symbol before or after the company name. Look out for tricks such as substituting the number "1" for the letter "l" in a web address (for example, www.paypa1.com instead of www.paypal.com).

An example of a phishing site.

Ways to prevent phishing scams: Incorrect company name. Often the web address of a phishing site looks correct, but actually contains a common misspelling of the company name or a character or symbol before or after the company name. Look out for tricks such as substituting the number "1" for the letter "l" in a web address (for example, www.paypa1.com instead of www.paypal.com).

- Missing slash. To verify that you're on a legitimate Yahoo! site, make sure a forward slash (" / ") appears after "yahoo.com" in the Address bar

- If you not sure if a site is authentic, don't use your real password to sign in. If you enter a fake password and appear to be signed in, you're likely on a phishing site. Do not enter any more information; close your browser. Keep in mind, though, that some phishing sites automatically display an error message regardless of the password you enter. So, just because your fake password is rejected, don't assume the site is legitimate.

- Use a web browser with anti-phishing detection. eg, Internet explorer and Mozilla firefox

Tuesday, February 24, 2009

How E-commerce can reduce cycle time, improve employees's empowerment and facilitate customer support

With the increasing usage of internet and the advancement of technology, more and more people are starting to see the convenience of e-commerce. With e-commerce, people can make purchases without even stepping out of their house. What differentiate e-commerce apart from the conventional way of selling and buying is reduced cycle time and the convenience.

Cycle time is the time where a process needed to complete from beginning until the end of it. This system can help to reduce the cycle time by creating a fast and direct system without wasting any valuable time. For example, customers can get immediate responses from the dealers or the supplier once the customers request to purchase the items on the system. From the system, it will immediately get to the suppliers without wasting time and money to go to the shop and they can make the payment online through credit cards. After the company receives the orders and payment, they will prepares the items accordingly and send it to the customers. Thus, the e-commerce can reduce the cycle time of this process.

Besides reduced cycle time, e-commerce allows employees to make decisions. Empowerment by management to employees (especially customer service) can react quickly to solve customers demands or problems. They also need to check on the system and process any transactions that requested by the customers. With empowerment, customer satisfaction will be increased due to the swift respond from the company personnel and thus increasing the usage of e-commerce.

Other than that, e-commerce is basically done on web sites. The advantage of the web site is that it can serve several purposes to facilitate the buying process. An added advantage to e-commerce is that customers can also seek help and advice from customer support. Any doubts and uncertainty can be cleared and verified via the customer support.

Cycle time is the time where a process needed to complete from beginning until the end of it. This system can help to reduce the cycle time by creating a fast and direct system without wasting any valuable time. For example, customers can get immediate responses from the dealers or the supplier once the customers request to purchase the items on the system. From the system, it will immediately get to the suppliers without wasting time and money to go to the shop and they can make the payment online through credit cards. After the company receives the orders and payment, they will prepares the items accordingly and send it to the customers. Thus, the e-commerce can reduce the cycle time of this process.

Besides reduced cycle time, e-commerce allows employees to make decisions. Empowerment by management to employees (especially customer service) can react quickly to solve customers demands or problems. They also need to check on the system and process any transactions that requested by the customers. With empowerment, customer satisfaction will be increased due to the swift respond from the company personnel and thus increasing the usage of e-commerce.

Other than that, e-commerce is basically done on web sites. The advantage of the web site is that it can serve several purposes to facilitate the buying process. An added advantage to e-commerce is that customers can also seek help and advice from customer support. Any doubts and uncertainty can be cleared and verified via the customer support.

Sunday, February 22, 2009

Electronic currency

What Does Electronic Currency Trading Mean?It is a method of trading currencies through an online brokerage account. Electronic currency trading involves converting base currency to a foreign currency at the market exchange rates through an online brokerage account. And Electronic currency traders use analysis based on technical and fundamental indicators to help them forecast the movement of the currency pair being traded. Because currency trading by this method is wholly electronic, execution speeds are extremely fast, allowing the trader to quickly buy and sell currencies to cut losses and take profits at a moment's notice.

What Does Electronic Currency Trading Mean?It is a method of trading currencies through an online brokerage account. Electronic currency trading involves converting base currency to a foreign currency at the market exchange rates through an online brokerage account. And Electronic currency traders use analysis based on technical and fundamental indicators to help them forecast the movement of the currency pair being traded. Because currency trading by this method is wholly electronic, execution speeds are extremely fast, allowing the trader to quickly buy and sell currencies to cut losses and take profits at a moment's notice. Technically electronic or digital money is a representation, or a system of debits and credits, used (but not limited to this) to exchange value, within another system, or itself as a stand alone system, online or offline. Also sometimes the term electronic money is used to refer to the provider itself. A private currency may use gold to provide extra security, such as digital gold currency. An e-currency system may be fully backed by gold (like e-gold and c-gold), non-gold backed, or both gold and non-gold backed (like e-Bullion and Liberty Reserve). Also, some private organizations, such as the US military use private currencies such as Eagle Cash.

Many systems will sell their electronic currency directly to the end user, such as Paypal and WebMoney, but other systems, such as e-gold, sell only through third party digital currency exchangers.

Many systems will sell their electronic currency directly to the end user, such as Paypal and WebMoney, but other systems, such as e-gold, sell only through third party digital currency exchangers.

In the use of off-line electronic money, the merchant does not need to interact with the bank before accepting a coin from the user. Instead he can collect multiple coins Spent by users and Deposit them later with the bank. In principle this could be done off-line, i.e. the merchant could go to the bank with his storage media to exchange e-cash for cash. Nevertheless the merchant is guaranteed that the user's e-coin will either be accepted by the bank, or the bank will be able to identify and punish the cheating user. In this way a user is prevented from spending the same coin twice (double-spending). Off-line e-cash schemes also need to protect against cheating merchants, i.e. merchants that want to deposit a coin twice (and then blame the user).

In the use of off-line electronic money, the merchant does not need to interact with the bank before accepting a coin from the user. Instead he can collect multiple coins Spent by users and Deposit them later with the bank. In principle this could be done off-line, i.e. the merchant could go to the bank with his storage media to exchange e-cash for cash. Nevertheless the merchant is guaranteed that the user's e-coin will either be accepted by the bank, or the bank will be able to identify and punish the cheating user. In this way a user is prevented from spending the same coin twice (double-spending). Off-line e-cash schemes also need to protect against cheating merchants, i.e. merchants that want to deposit a coin twice (and then blame the user).The main focuses of digital cash development are 1) being able to use it through a wider range of hardware such as secured credit cards; and 2) linked bank accounts that would generally be used over an internet means, for exchange with a secure micropayment system such as in large corporations (PayPal).

Theoretical developments in the area of decentralized money are underway that may rival traditional, centralized money. Systems of accounting such as Altruistic Economics are emerging that are entirely electronic, and can be more efficient and more realistic because they do not assume a zero-sum transaction model.

Corporate blogging

Blogs - an abbreviation of 'weblogs' - are published on the web, typically as microsites standing by themselves but today also as parts of traditional web sites. They reflect the interests, thoughts and opinions of the person, sometimes persons, publishing the blog. Blogs are characterized by frequent updates, an informal tone and many links to other blogs and web sites.A corporate blog is a blog published by or with the support of an organization to reach that organization's goals. In external communications the potential benefits include strengthened relationships with important target groups and the positioning of the publishing organization (or individuals within it) as industry experts. Internally blogs are generally referred to as tools for collaboration and knowledge management.

Blogging has caused quite a buzz. From political activists to aspiring novelists, industry pros and avid hobbyists, everyone seems to be starting a blog. Recent articles in Business Week and Forbes demonstrate how even the mainstream media is taking notice of their unprecedented growth and increasing effect on our society. But can corporate blogging really deliver measurable return-on-investment for your business?

In this paper, we address the following questions: why would a company want to start blogging? Who should blog? What makes a blog successful? And how can companies use this type of website to facilitate positive business growth?

To find the answers to these questions, we surveyed bloggers at hundreds of companies and conducted in-depth interviews with representatives from six corporations currently leading the way in blogging activities. What we discovered was that for the majority of our survey sample —including some of today’s largest corporations and scrappiest underdogs —corporate blogs are, in fact, living up to all the hype.

Corporate blogs are giving established companies and obscure brands alike the ability to connect with their audiences on a more personal level, build trust, collect valuable feedback and foster strengthened business relationships. More importantly, these companies are enjoying tangible returns in their blogging investment in the form of increased sales, partnerships, business opportunities, press coverage and lead generation.

Companies that employ a well thought out blogging strategy encourage the strongest community goodwill, and that goodwill, in turn, promotes significant marketing and sales gains. It is said that success breeds success.

This holds very true for successful blogs. There is chain reaction that begins with a real desire on the part of the blogger to provide value and connect with their audience. The blogger shares useful and engaging content —the latest information, help, discussion topics and ideas. The way the audience responds to that content is key.

When customers start commenting, posting or tracking back to a blogging community, it can have a viral effect —spreading out across the blogosphere. In addition, companies that harness their customers’ knowledge and ideas find better ways to satisfy their needs and wants, thus facilitating goodwill in the community. For example, it is a common practice in blogging to provide a link back to a thought originator, which is valuable because backlinks are a way that search engines distinguish the order of the editorial rankings.

Higher search engine rankings translate into significantly higher web site traffic and more sales leads. Thus, successful blogging breeds success in other marketing and sales initiatives.

Greater word-of-mouth buzz on- and offline, higher search engine rankings, increased press coverage and superior lead generation are just some of the potential benefits of blogging in a corporate setting. In the next chapters, we will examine the blogging strategies of a number of companies, and learn how they are already reaping the rewards of their investment in corporate blogging.

Backbone Media, Inc. Grants permission for re-use of the content herein with the understanding that the user will cite the authors and include a reference to Backbone Media, Inc. with the following ink: http://www.backbonemedia.com/.

Monday, February 16, 2009

An example of an E-Commerce success and its causes

If you picked eBay, its probably because that’s what most people think about when they are considering selling something online. And for good reason! eBay is one of the most popular shopping areas on the internet with millions of registered users all over the world. In 2004, eBay had revenues of around $3.2 billion dollars. Between $7 - $8 Billion is run through eBay's platform every quarter. What was founded in 1995 as a hobby website has grown to a multi-billion dollar website. Talk about your niche markets! Every hour eBay registers 3,000 - 4,000 new users. More than 724,000 people report that eBay is their primary or secondary source of income and another 1.5 million say eBay is a supplemental source of income.

When one is thinking about starting a business, the primary rules for success are Location, Location, Location. If you are doing business on eBay, you are tapping into not only the most popular marketplace on the planet, but one that demands, and has the attention of millions of shoppers. There is no better location anywhere to sell your goods and services for incredibly reasonable rates. When you add in the convenience of PayPal, BidPay, the search tools, and the flexibility of how you can put together your auctions and business, there really is no comparable alternative that makes good business sense.

The stock performance may be all out of proportion, but the fact is, eBay has stumbled onto the next great E-commerce category: collectibles. It was founded in 1995 by Pierre Omidyar, a 31-year-old software developer who wanted to help his fiancee trade Pez dispensers online. He created a small auction site, charging just a tiny fee and commission for each listing. The risks were minimal since eBay acts only as an intermediary; the parties arrange delivery on their own. The model far exceeded Omidyar's expectations, and within a year he quit his day job. This year he hired as CEO Meg Whitman, who previously oversaw brands like Mr. Potato head and Teletubbies for Hasbro.

eBay's success is testimony to the Internet's ability to transform one person's junk--taxidermy animals or Fisher-Price toys--into another's treasure by matching sellers with a huge audience of buyers. Domenica Brockman, a Brooklyn antiques dealer, got hooked after she was able to sell an obscure Depression-era green-glass pitcher--that she paid $3 for--to a collector for $150. "I never would have gotten that price for it in my store," she says.

This enthusiasm has made eBay the leader in the online collectibles market. It was the fifth-most-visited Website in August, according to Media Metrix, an Internet-tracking company. "More time is spent in eBay's community than on either AOL.com's or Walt Disney's Website," says Mary Meeker, an analyst at Morgan Stanley Dean Witter. This growth has been driven by word of mouth, since until recently the company has avoided advertising. "Every auction and every buyer begets another auction and another buyer," says analyst Mitch Bartlett of Dain Rauscher Wessels.

When you really think about it, it all comes down to flexibility, cost, and potential business success. No other internet location offers the opportunities for success that eBay does. No other internet marketplace will provide you with the continuous exposure and stream of customers that eBay does each and every day and night of the year. "I've shopped for antique clocks listed by German sellers at 2:00 AM. I've visited eBay auctions in Holland, England, Italy. Where else can you go to see, buy and sell with such a worldwide focus"?

eBay's success is not in what they sell, but in what you and I buy and sell. It's a marketplace with over $30 Billion dollars worth of goods changing hands every year. The big numbers should not be viewed as competition, but rather, your opportunity for success.

Sunday, February 15, 2009

The threat of online security: How safe is our data?

Online security is often a major cause that held back the development of e-commerces. Consumers tend to worry about their personal data to be leak out and used in negative purposes. On another hand, organizations are worried about the online security too. According to Information Security Survey, 2000, companies conducting either B2B or B2C e-commerce experience a significant higher rate of both insider and outsider security breaches than companies not conducting e-commerce.

However, as the technology grow along quickly, the security requirement has been increased to protect the safety of the information. The security requirements are summarized into 3 category namely Confidentiality, Integrity, and Authentication.

Confidentiality makes sure that a message is kept confidential or secret such that only intended recipient can read it. It able to eliminates the consumers' worry about their personal data to be fallen to unattended personnel. Encryption is a favourite tool to provided confidentiality.

Integrity is aiming to make sure that if the content of a message is altered, the receiver can detect it. Thus, when a payment information is changed, the message is no longer valid.

Authentication is about verify identity. Where the identity of the company can be verified before carrying out a transaction. In an open c-commerce system, a digital certificate is employed to satisfy the authentication requirement. Besides, it ensures that the involved parties cannot deny the occurrence of a transaction.

However, as the technology grow along quickly, the security requirement has been increased to protect the safety of the information. The security requirements are summarized into 3 category namely Confidentiality, Integrity, and Authentication.

Confidentiality makes sure that a message is kept confidential or secret such that only intended recipient can read it. It able to eliminates the consumers' worry about their personal data to be fallen to unattended personnel. Encryption is a favourite tool to provided confidentiality.

Integrity is aiming to make sure that if the content of a message is altered, the receiver can detect it. Thus, when a payment information is changed, the message is no longer valid.

Authentication is about verify identity. Where the identity of the company can be verified before carrying out a transaction. In an open c-commerce system, a digital certificate is employed to satisfy the authentication requirement. Besides, it ensures that the involved parties cannot deny the occurrence of a transaction.

Identify and compare the revenue model for Google, Amazon.com and eBay.

Revenue model is describing on how a firm earns revenue, generates profit and produce a superior return on invested capital.

Google is practicing an advertising revenue model. where it serves as a Web site that offers its users content, services and products, or provides a forum for advertisements and receives fees from the advertisers. Google website is able to attract the greatest viewership or that have a higher specialized, differentiated viewership and are able to retain user attention, in other word, to provide "stickiness". Thus, it is able to charge higher advertising rates. Google derives significant amount of revenue from selling advertising such as banner ads. For instances, The principal products and services provided is Google AdWords, which is a pay-per-click advertising program. Google designed it to allow the advertisers to present advertisements to people at the instant the people are looking for information related to what the advertiser has to offer.

Google is practicing an advertising revenue model. where it serves as a Web site that offers its users content, services and products, or provides a forum for advertisements and receives fees from the advertisers. Google website is able to attract the greatest viewership or that have a higher specialized, differentiated viewership and are able to retain user attention, in other word, to provide "stickiness". Thus, it is able to charge higher advertising rates. Google derives significant amount of revenue from selling advertising such as banner ads. For instances, The principal products and services provided is Google AdWords, which is a pay-per-click advertising program. Google designed it to allow the advertisers to present advertisements to people at the instant the people are looking for information related to what the advertiser has to offer.

Amazon.com is using the sales revenue model. the company derive revenue by selling goods, information, or services to customers. Amazon.com sells books, music and other products such as toys, wireless phones, cameras, and video games to consumers. Typically, Amazon.com is a B2C (Business to Consumer) e-commerce in which business sells already manufactured products to the consumers directly on the Internet. Books are listed under different sections for ease of searching. Besides, a search facility is available for searching books according to user input. Besides, Amazon.com also make use of data mining techniques to promote the selling of books. Later, books are sent by mail or courier, whichever the customer prefers.

eBay is a company practicing the transaction fee revenue model. eBay receive a fee for enabling or executing a transaction. eBay provides the world's largest online trading service by means of online auction. It creates an online auction marketplace and receive a small transaction fee from seller if the seller is successful in selling the item.

Sunday, February 8, 2009

The application of third party certification programme in Malaysia

The most famous application of 3rd party certification program in Malaysia is provided by the MSC Trustgate.com Sdn Bhd. MSC Trustgate.com Sdn Bhd was incorporated in 1999 and is a licensed Certification Authority (CA) under the operation of the Multimedia Super Corridor. Certification Authority is the body given the license to operate as a trusted third party in the issuance of digital certificates.

The most famous application of 3rd party certification program in Malaysia is provided by the MSC Trustgate.com Sdn Bhd. MSC Trustgate.com Sdn Bhd was incorporated in 1999 and is a licensed Certification Authority (CA) under the operation of the Multimedia Super Corridor. Certification Authority is the body given the license to operate as a trusted third party in the issuance of digital certificates.The objective of MSC Trustgate is to secure the open network communications from both locally and across the ASEAN region. Trustgate provide digital certification services such as digital certificates, cryptographic products and software development. The products and services of Trustgate are SSL Certificate, Managed PKI, Personal ID, MyTRUST, MyKAD ID, SSL VPN, Managed Security Services, VeriSign Certified Training and Application Development. The vision of Trustgate is to enable organizations to conduct their business securely over the internet, as much as what they have been enjoying in the physical world.

Digital certificate usually attach to an e-mail message or an embedded program in a web page that verifies that user or website is who they claim to be. The common functions of a digital certificate are user authentication, encryption and digital signatures. User authentication provides other security than using username and password. Its session management is stronger. Encryption can make the data transmission secured by using the information encrypted. The intended recipient of the data is only person to receive the message. Digital signatures are like the hand signature in the digital world. It can ensure the integrity of the data.

By using the digital certificate, the users will be able to make transaction on the internet without fear of having the personal data being stolen, information contaminated by third parties, and the transacting party denying any commercial commitment with the users. Furthermore, the digital certificates can assist the development of greater internet based activities.

The Website of MSC Trustgate:http://www.msctrustgate.com/

The Website of MSC Trustgate:http://www.msctrustgate.com/

The history and evolution of E-commerce

History of ecommerce dates back to the invention of the very old notion of “sell and buy”, electricity, cables, computers, modems, and the Internet. At first, the term ecommerce meant the process of execution of commercial transactions electronically with the help of the leading technologies such as Electronic Data Interchange (EDI) and Electronic Funds Transfer (EFT) which gave an opportunity for users to exchange business information and do electronic transactions. The ability to use these technologies appeared in the late 1970s and allowed business companies and organizations to send commercial documentation electronically.

Although the Internet began to advance in popularity among the general public in 1994, it took approximately four years to develop the security protocols (for example, HTTP) and DSL which allowed rapid access and a persistent connection to the Internet. In 2000 a great number of business companies in the United States and Western Europe represented their services in the World Wide Web. At this time the meaning of the word ecommerce was changed. People began to define the term ecommerce as the process of purchasing of available goods and services over the Internet using secure connections and electronic payment services. Although the dot-com collapse in 2000 led to unfortunate results and many of ecommerce companies disappeared, the “brick and mortar” retailers recognized the advantages of electronic commerce and began to add such capabilities to their web sites (e.g., after the online grocery store Webvan came to ruin, two supermarket chains, Albertsons and Safeway, began to use ecommerce to enable their customers to buy groceries online). By the end of 2001, the largest form of ecommerce, Business-to-Business (B2B) model, had around $700 billion in transactions. History of ecommerce is unthinkable without Amazon and Ebay which were among the first Internet companies to allow electronic transactions. Thanks to their founders we now have a handsome ecommerce sector and enjoy the buying and selling advantages of the Internet. Currently there are 5 largest and most famous worldwide Internet retailers: Amazon, Dell, Staples, Office Depot and Hewlett Packard. According to statistics, the most popular categories of products sold in the World Wide Web are music, books, computers, office supplies and other consumer electronics.One more company which has contributed much to the process of ecommerce development is Dell Inc., an American company located in Texas, which stands third in computer sales within the industry behind Hewlett-Packard and Acer.

Year and Event:

1984

EDI, or electronic data interchange, was standardized through ASC X12. This guaranteed that companies would be able to complete transactions with one another reliably.

1992

Compuserve offers online retail products to its customers. This gives people the first chance to buy things off their computer.

1994

Netscape arrived. Providing users a simple browser to surf the Internet and a safe online transaction technology called Secure Sockets Layer.

1995

Two of the biggest names in e-commerce are launched: Amazon.com and eBay.com.

1998

DSL, or Digital Subscriber Line, provides fast, always-on Internet service to subscribers across California. This prompts people to spend more time, and money, online.

1999

Retail spending over the Internet reaches $20 billion, according to Business.com.

2000

The U.S government extended the moratorium on Internet taxes until at least 2005.

1984

EDI, or electronic data interchange, was standardized through ASC X12. This guaranteed that companies would be able to complete transactions with one another reliably.

1992

Compuserve offers online retail products to its customers. This gives people the first chance to buy things off their computer.

1994

Netscape arrived. Providing users a simple browser to surf the Internet and a safe online transaction technology called Secure Sockets Layer.

1995

Two of the biggest names in e-commerce are launched: Amazon.com and eBay.com.

1998

DSL, or Digital Subscriber Line, provides fast, always-on Internet service to subscribers across California. This prompts people to spend more time, and money, online.

1999

Retail spending over the Internet reaches $20 billion, according to Business.com.

2000

The U.S government extended the moratorium on Internet taxes until at least 2005.

Friday, February 6, 2009

Yu Ern

Hello, i'm yu ern. currently, i'm staying in Sg Long, Kajang. i'm an undergraduate in UTAR Business Aministration in Entrepreneurship Course. my hobbies are eating, and travelling. However, to avoid continue gaining weight...i really have to control it better.

i'm not a IT expert, and my friends are keep laughing at me...it's ok to me!! So, most of my time i spend in Internet is chatting, surfing information and playing mini games.

The top 5 website i visit most are

1. http://www.msn.com/

2. http://www.friendster.com/

3. http://www.cn.yahoo.com/

4. http://www.123greetings.com/

5. http://www.y8.com/

i'm not a IT expert, and my friends are keep laughing at me...it's ok to me!! So, most of my time i spend in Internet is chatting, surfing information and playing mini games.

The top 5 website i visit most are

1. http://www.msn.com/

2. http://www.friendster.com/

3. http://www.cn.yahoo.com/

4. http://www.123greetings.com/

5. http://www.y8.com/

Thursday, February 5, 2009

Kah Yen

hihi... This is the first time i post a blog.... actually if not some reasons i really wont post any blog, cause lazy........^^v but nevermind treat this as a good starting point to me.

My name is Yen, or you can call me "shi fu" this name come from my ALL BEST BEST!! friend... thanks to them. i come from HILL CITY, Ipoh, Perak, a nice place...i now is study at UTAR in Sg,Long...i like to play everything, any plan just INVITE ME!!!!!!!! but make sure i am free... hahahaha....

The following is my top 5 visited website

http://www.tuku.cc/

http://www.happytreefriends.com/

http://www.yahoo.com/

http://www.zanba.com/

http://www.google.com/

My name is Yen, or you can call me "shi fu" this name come from my ALL BEST BEST!! friend... thanks to them. i come from HILL CITY, Ipoh, Perak, a nice place...i now is study at UTAR in Sg,Long...i like to play everything, any plan just INVITE ME!!!!!!!! but make sure i am free... hahahaha....

The following is my top 5 visited website

http://www.tuku.cc/

http://www.happytreefriends.com/

http://www.yahoo.com/

http://www.zanba.com/

http://www.google.com/

Dexter Yin

Hai this is my 1st time posting a blog, never thought of starting a blog but this is for e-commerce so i guess i can do it. Im Dexter and welcome to my part of the blog, sharing a blog with my fellow classmates is so awesome. Andy keeps telling me to start on the blog already so, here it is!!

Hai this is my 1st time posting a blog, never thought of starting a blog but this is for e-commerce so i guess i can do it. Im Dexter and welcome to my part of the blog, sharing a blog with my fellow classmates is so awesome. Andy keeps telling me to start on the blog already so, here it is!!Lets start by introducing myself, i'm a business student majoring in entrepreneurship. I am very veery lazy but i am very fortunate to have friends that help me alot. I love u guys.. evrybody in ENT04!!

Other than that, im a typical teen that enjoy doing the same things that the next person would. Like hanging out, eating together, or going to the "library", and surfing the net. Speaking of which, let me introduce my top 5 websites that i visit the most :)

#1 - www.crunchyroll.com

This is where i watch some of my animes. If u dont know what animes are, u should go bang a wall, OR u could click on the link to find out =P

#2 - www.facebook.com

This is where i play poker.

This is where i play poker.#3 - www.google.com

This is my search engine.

This is my search engine.#4 - www.yahoo.com

Another search engine. This is my homepage.

Another search engine. This is my homepage.#5 - www.kennysia.com

The only blog i follow is Kenny's.

The only blog i follow is Kenny's.Thats all for post number 1. Im sure more will come, considering i have more tutorial questions =D

Tuesday, February 3, 2009

Andy

Andy's Profile

Andy's Profile Hi, everyone.

I am here to introduce myself. I am Wong Chia Yau and you all can call me Andy, 22 years old and I come from Taiping, Perak. Before study in Utar I was a Tarcian . I am a year 3 semester 1 student of Bachelor of Business Administration (Hons) Entrepreneurship. My hobbies is travelling, playing badminton, chatting, play soduko and hiking.

The top 5 websites that I regular visits are:

1. http://www.friendster.com/

I will update my profile and get to know my friends' latest news.

2. http://www.msn.com/

I will chatting with friends and reply email.

3. http://www.google.com/

I will use this as a search engine.

4. http://www.shockwave.com/gamelanding/dailysudoku.jsp

I will enjoy the latest games here.

5. http://hdzone.org/

I always online downloading drama and search for new drama!

The top 5 internet activities that I regular do are:

-Mailings

-Search for information

-Download music and drama

-Watch video or flash movie

Subscribe to:

Comments (Atom)

.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}